The ingredient aquaculture can’t outgrow

No food sector has grown as fast as aquaculture over the past three decades. Aquaculture surpassed capture fisheries in 2022 and volumes have reached unprecedented levels. By 2034, the sector is expected to supply 61 percent of all aquatic products consumed by humans.

That expansion reverberates along the entire supply chain, from hatcheries to processing facilities and, most critically, feed – the largest cost factor in any fed aquaculture model. While modern aquafeed draws on dozens of new ingredients, one component remains the industry’s weak spot.

A finite resource under growing pressure

Fish oil is the industry's primary source of EPA and DHA – the long-chain omega-3 fatty acids that drive growth, health, and flesh quality in farmed salmon, shrimp, and marine fish. Over time, omega-3 content has also become a central selling point on the consumer side, with health claims lifting demand worldwide.

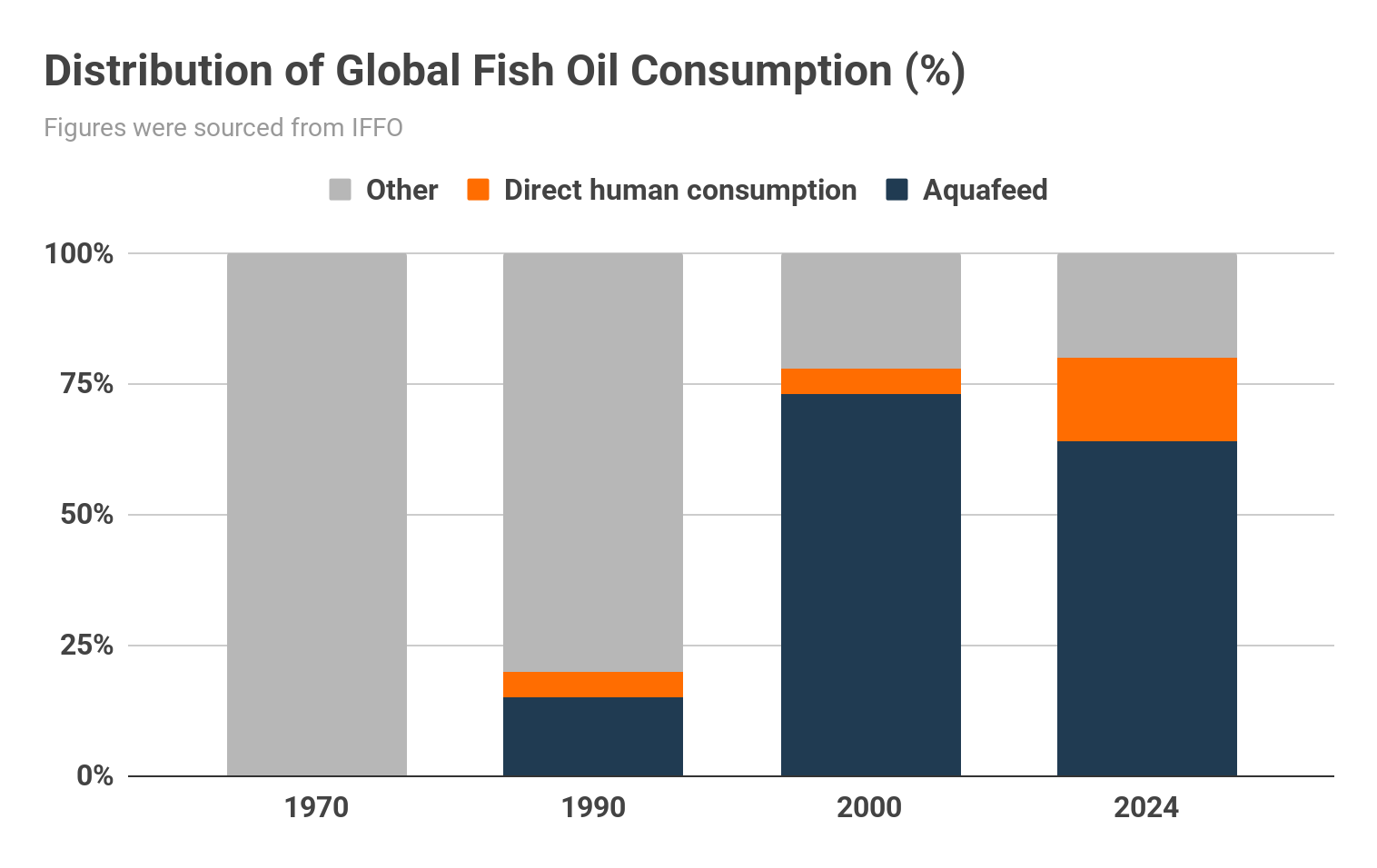

The oil itself comes from small pelagic fish "reduced" into oil. Aquaculture already absorbs around 77 percent of the global supply, with Atlantic salmon alone accounting for roughly 60 percent. The species that need it most are also the fastest growing in the sector:

- Salmon farming is expected to grow 4 to 6 percent annually through 2030.

- Shrimp and prawn production is projected to grow at an implied rate of about 3.3 percent per year up to 2034.

All of this points to rising demand for a finite resource that has already shown its limits. The supply rests on a narrow geographic and biological base, with Peru alone accounting for roughly 20 percent of global output.

The compounding risks of climate and geopolitics

The current model exposes the industry to unpredictable external shocks, making reliance on marine ingredients increasingly unsustainable:

- Climate Volatility: In March 2024, fish oil traded at €6,400 per tonne, roughly five times its historical average. The cause was an El Niño event that forced Peru to cancel its first fishing season of the year. For the aquaculture industry, this price shock was a bitter reminder of its dependence on a single, geographically concentrated resource. As climatic events are expected to become more frequent, the industry is facing an era of uncertainty and volatility surrounding this single resource. In fact, there is now mounting evidence that a new El-Niño event is taking shape in the Pacific and recent reports highlight that it is developing faster than anticipated and has the potential to be more severe than past events.

- Geopolitical & Regulatory Risks: Above sea-level, geopolitics adds another layer of complexity. In the North East Atlantic, coastal nations have repeatedly failed to agree on quotas for pelagic fish, leading to the suspension of MSC certifications for blue whiting, mackerel, and herring in 2019 and 2020. With these events, aquafeed producers committed to certified sourcing are facing a steadily narrowing pool of certified options.

Why fish oil remains so difficult to replace

Over the past decades, much of the industry's fish meal has been successfully swapped for terrestrial ingredients – a shift Hatch Blue has explored in a report on emerging protein ingredients. However, replacing fish oil has proved much more challenging due to biological and structural ceilings:

- The Nutritional Limit of Conventional Oils: Conventional land-based oils such as rapeseed and sunflower oil do not supply adequate levels of EPA and DHA. Research shows that up to a third of fish oil can be replaced with these vegetable oils without apparent impact on fish growth. Beyond that threshold, substitution begins to affect animal performance and health.

- Impact on product composition: Partial substitution over the years has directly reflected in the nutritional composition of final products. In Scottish Atlantic salmon, EPA and DHA levels in the flesh halved between 2006 and 2015. Continued substitution with conventional vegetable oils would further reduce omega-3 levels and risk compromising animal performance.

- The Limits of By-Products: To ease the pressure, producers have increasingly turned to processing waste. By-products – mainly from pangasius and farmed salmon – now supply around 51 percent of global fish oil. However, further expansion is constrained by processing infrastructure and reliable feedstock flows, meaning by-products are unlikely to scale to meet projected future requirements.

Scaling the next generation of aquatic nutrition

The challenges outlined above make clear that the fed-aquaculture industry cannot sustain its projected growth on fish oil alone. Building resilience against climate shocks, geopolitical disruption, and market volatility into the aquafeed supply chain is a necessity.

This does not mean fish oil will disappear from aquaculture feeds; it will remain an important ingredient, particularly for high-value species at critical life stages. But the industry's current dependence on a single, constrained source of EPA and DHA is a vulnerability. Diversification requires that alternative sources are tested, validated, and scaled now, so they are viable when the industry needs them most.

Several promising alternatives are already in various stages of development:

- Microalgae cultivated under controlled conditions to produce EPA and DHA directly

- Single-cell oils derived from heterotrophic fermentation of microorganisms

- Genetically modified oilseed crops engineered to produce long-chain omega-3s

- Lipids extracted from insects

Each offers a different profile of advantages and trade-offs in terms of nutritional performance, scalability, cost, and environmental footprint. Hatch Blue continues to monitor this landscape closely through our advisory and investment work across feed innovation and emerging ingredient platforms, with growing attention to how alternative lipids are progressing from technical promise to commercial relevance.

If you are developing solutions or navigating supply chain transitions in the aquafeed space, we invite you to connect with our team to explore the future of aquatic nutrition.

Goncalo Santos, Director, Hatch Blue - [21 May 2026]

Related Posts

Fjord-born innovations: Showcasing Sustainability at the Nordic Silicon Valley of Aquaculture

.png)

Winter wounds: innovative solutions to improve fish welfare in salmon farming

Hatch Blue mobilises for a momentous Aqua Nor